These Stand the Test of Time

Some things never change

This might be the most interesting time in financial history. One day we’re in a recession, and the next day the definition of recession changes. One day crypto will change the world, and the next day the leading mind in crypto is a League of Legends playing liar who makes all of the crypto “bros” worldwide question everything they know. Every day the momentum in the financial world is swinging from one side to the other. It can be tough to keep up when it feels like everything is changing. But, I’m here to say nothing is really changing.

Let me explain.

CNBC recently interviewed 5 CEOs of major companies about their perspective of the “pending” recession in 2023, and 4 out of 5 said there were signs of recession. The lone CEO who didn’t see recession was Scott Kirby of United Airlines, who said “If I didn’t watch CNBC in the morning – which I do – the word recession wouldn’t be in my vocabulary.” It was a bold take by Scott to not only go against his fellow CEOs, but also call out the show he’s being interviewed on.

The same day the CEOs of Goldman Sachs and Bank of America conducted interviews where they also warned of a looming recession, with many of these leaders saying more job cuts could be coming. Easy to see why people could be scared. These are the top leaders at companies that would have insight into consumer debt and spending, as well as material costs.

It wasn’t just these interviews either. Every news headline, move by the Fed, and political speech swing the pendulum towards fear. But, this isn’t new! The idea of the media and our leaders changing the temperature in the room has been going on for decades now. If a leading “expert” on any topic says something positive, the next day everything seems great; and vice-versa. Now, I don’t blame top leaders for speaking out sometimes. In the financial world, there are major institutions that need to know what’s going on. Hedge funds, financial advisors, and other companies need this insight to better manage investor funds and make great products. However, for everyday people like you and me, these comments are often insignificant. This isn’t the first time we’ll see headlines laden with fear, and it won’t be the last.

To get ahead of this and make you feel more secure with the economy, there are a few basic financial items we all need to do. Doing these things will ensure that your financial well-being (aka your money) will stand strong against the ever-changing winds. I call this the Personal Finance Starter Pack™. Let’s begin.

The first item in the Starter Pack is the budget. More specifically, it’s spending less than you make. Take a piece of paper, or spreadsheet, and write how much you bring home each month. Then, subtract all of your expenses. If you have a positive number, you’re off to a great start! If it’s a negative, start to dive into what you’re spending on. Look at your credit card statement to see where your money is going. You might actually be surprised when you take a closer look at what you can easily live without and take out. Also, shameless plug here, but this template is a great way to start your budget if you don’t have one.

Next up is the emergency fund. The basic idea behind this is quite simple too — if an emergency happens (losing your job, big ticket item breaks, etc.), you’re covered. Ideally, this fund covers 3-6 months of your expenses. If you get really worried about not having things covered, increase this to a year. To find your ideal emergency fund amount, take your expenses and multiply by the number of months you want in the fund. I also think focusing on your higher priority expenses (rent, food, utilities) should be the basis of your emergency fund, not your eating out budget (sorry Kelsey). If things get really rough, PF Chang’s will have to wait.

The final item in the Starter Pack is retirement investing. No matter what season you’re in, you should be investing enough in your 401K to get your employer’s match. If you can do more, max out a Roth IRA and then go back and contribute more to your 401K. Most importantly, even if you think we’re in a recession, don’t stop investing. Each contribution today adds even more to that retirement nest egg of yours in the future. This is especially important today, as a top Google search in 2022 was “Should I stop 401K contributions?”. People are worried, but since you’re reading this, you don’t have to be.

Now, you might be reading all of this and say: “Zane, people everywhere are losing their job and I’m next!” To which I’d ask you right back, “Are they?”.

The November Bureau of Labor Statistics data showed fewer new claims for unemployment than the previous month. There are also 1.7 jobs for every 1 worker. This is in contrast to a 127% MoM spike in job cuts, primarily driven by the tech sector. Upon further analyzing this data, it suggests that workers who are losing their job are not looking for new ones.

So, after reading this I ask again: “Do you need to be worried?”

What I’m getting at, is that this isn’t the last time we’ll see job cuts. Even if you were to lose your job, there are likely jobs available for you if you seek them out. This is positive news!

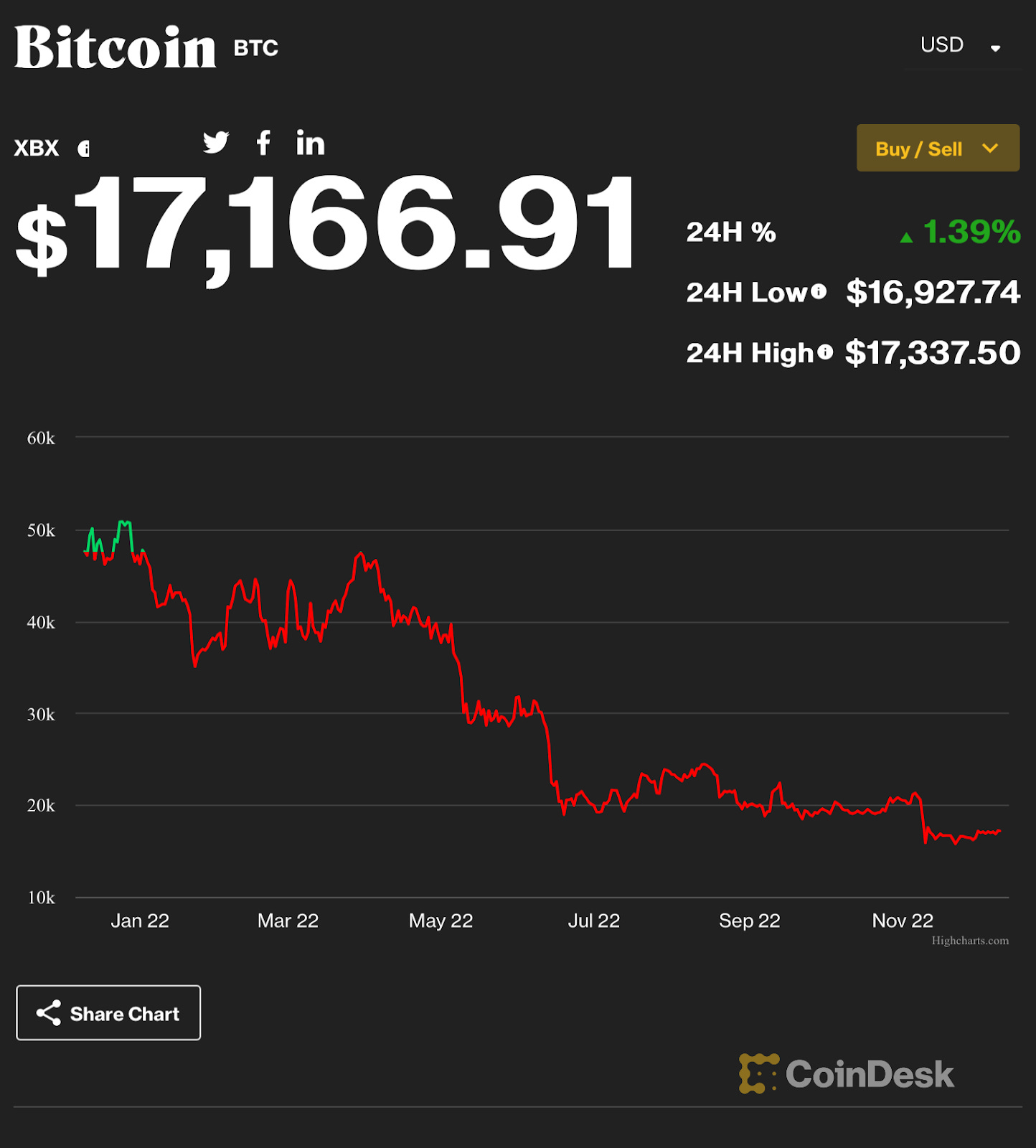

Now, another thing that adds to the story of today is the shiny new thing, specifically the “get rich quick” asset of the past few years: crypto. In November of 2021 Bitcoin hit an all-time high of $65,000. Yet, since then the leading cryptocurrency has fallen off, leading many to lose everything they had.

Source: CoinDesk

Not only that, but we’ve also seen a flurry of stories about two acronyms: FTX & SBF. The story of Sam Bankman-Fried is a case study of greed and fooling others. For investors, it’s another story of chasing the shiny new thing. Looking back through history, how often has the new kid on the block helped retail investors (you & me) create and sustain long-term wealth? It’s unlikely you’ll pick the newest Amazon, Apple, or Tesla. Instead, stick with index funds instead of picking the hottest new stock. There have been many more debuting companies that tank then there are like the three I just mentioned.

All of this is to say that what we’re seeing today is the same idea dressed differently. The news will always make gloomy headlines and there will always be a shiny new “get rich” asset. Yet, what has also been consistent through time are the basics of personal finance: spend less than what you make, have an emergency fund, and consistently invest for retirement. Doing these three things will ensure you and your money will withstand the test of time.